First of all, I thank to Mr. VKSNathan who gave the idea for this article. (Click here to know the background). Now a days many home loan borrowers are opting a particular type of home loan from SBI which is called Max Gain. In this home loan, an Overdraft (OD) account is assigned to the customer’s home loan & any amount parked by customer is treated as loan repayment for the purpose of interest calculation, for the days, the amount stays there in that OD account. As on date following banks are offering similar types of home loan to their customers.

First of all, I thank to Mr. VKSNathan who gave the idea for this article. (Click here to know the background). Now a days many home loan borrowers are opting a particular type of home loan from SBI which is called Max Gain. In this home loan, an Overdraft (OD) account is assigned to the customer’s home loan & any amount parked by customer is treated as loan repayment for the purpose of interest calculation, for the days, the amount stays there in that OD account. As on date following banks are offering similar types of home loan to their customers.

SBI, IDBI, CITI, HSBC & Standard Chartered. Punjab National Bank can also be added in this list but it’s offering a combo of normal loan + OD. In this article, we are going to discuss only SBI Max Gain as in OD linked home loan, for the fact that the maximum business is with SBI & the most discussed topic on JI forum is also related to SBI Max Gain (click here).

What is an Overdraft account?

Before we discuss Max Gain, first understand, what is an OD account? All of us are well aware of functioning of an ordinary saving bank (SB) account. Here account operates between zero to positive & positive to zero. As we deposit our money, it’s used by bank & we get interest on our money from bank. In case of an OD account, bank first ask for a security & then assign a credit limit on the basis of the market value of that security. This security may be Fixed Deposits, Insurance Policies, National Saving Certificates, Shares, Mutual Fund units, house/commercial property etc. Now when we are using this assigned credit limit, the amount is going from zero to negative zone & when we are repaying, it’s coming from negative to zero. As we are using bank’s money in this case, the interest ‘ll be paid by us to bank. That’s how an OD account works.

So what is the correlation between Max Gain home loan & Over Draft account?

For Max Gain borrowers, SBI opens an Over Draft account where the Credit limit as discussed above is equal to the loan value assigned to the borrower. Here underlying security is the home you have purchased or constructed from that loan amount. Now as & when you are parking any surplus amount into this OD accout, the parked amount is treated as payment towards loan (effectively you are bringing down your loan liability from negative towards zero position) and thus the interest ‘ll be charged only on the difference amount i.e. total loan amount – parked surplus amount.

What is the primary benefit of Max Gain?

Well the primary benefit of MG is to keep your liquidity intact & still bringing down your interest outgo. To understand it better, please imagine a situation you are running a home loan of 30L Rs. & now you do have 2L Rs. with you to prepay. In normal home loan, your 2L Rs. ‘ll be accepted by bank & adjusted towards home loan & your amount is gone forever so no liquidity for you of that 2L Rs. amount. On the other hand, if you are MG customer, simply park those 2L Rs. in your MG account & your interest outgo ‘ll be lower from that month itself till those 2L Rs. or a part of it is there as surplus in MG account.

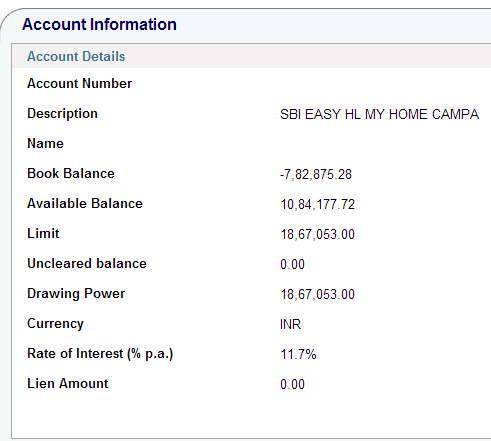

What is Drawing Power ?

Drawing Power is nothing but your as on date actual outstanding loan amount. Before final disbursal or start of loan repayment, it’s your sanctioned loan amount. Once your EMI starts, it’s your as on date actual outstanding loan amount. Please check Image below, Drawing Power here is 1867053 Rs. as on date. (Click here to understand it better)

What is Available balance?

Before final disbursal, it’s the sum of undisbursed amount + parked surplus & post final disbursal, it’s your parked surplus amount which is available to withdraw. Please check Image below, Available Balance here is 1084177.72 Rs. as on date. (Click here to understand it better)

What is Book balance?

It’s the adjusted loan amount arrived after deducting the Available Balance amount from Drawing Power. In your account statements it’s shown with a negative sign. Please check Image below, Book Balance here is – 782875.28 Rs. as on date. (Click here to understand it better)

Is there any extra interest for Max Gain?

No, the interest for home loan is same in SBI be it for normal home loan or for Max Gain.

I’m an existing SBI home loan customer. Can I convert my old term loan to Max Gain?

Yes, you can. Please contact your loan serving branch or RACPC for the required paperwork to be done. This may be an outdated info so please do check with your loan serving branch for current day rules on conversion.

I have taken the Max Gain for an Under Construction Property. Can I park surplus amount to save on interest outgo?

The answer is yes & no both. Yes you can park your surplus during under construction phase but do remember SBI is disbursing partially at this juncture & in case due to any emergency you want to liquidate your surplus, SBI ‘ll not allow the same. So park only that much surplus, you feel you ‘ll not need even in an extreme emergency.

If I’m parking some money on monthly basis or in lump sum, will my loan term come down or EMI go down?

No. Neither your EMI ‘ll come down nor your loan term. The only saving is in terms of interest outgo. To understand it better, Let’s assume a test case of loan amount 30L Rs. @ 10% Rate of Interest for 20Y term. The normal EMI for these nos. ‘ll be 28951 Rs. The break up of your EMI for first month ‘ll be 25000 Rs. interest & 3951 Rs. for principal repayment.

Now if you do have 2L Rs. surplus in the very first month & prepay the same as below –

Case – 1 Normal home loan

Your 2L Rs. is gone & outstanding loan amount ‘ll come to 2796049 & interest outgo ‘ll still be 25000 Rs. but the no. of months ‘ll come down from original 240 to 198 months.

Case – 2 Max Gain home loan

Your 2L Rs. are parked in that OD account & the interest for the very first month ‘ll be calculated on 28L Rs. & thus it ‘ll be 23334 & thus there‘ll be an interest saving of 1667 Rs. which‘ll remain available in your OD account as surplus along with your parked surplus 2L Rs. so for next month, the parked surplus amount ‘ll be 201667 Rs.

Please do note in case 2 above, Your loan term is still 240 months but the saving of interest ‘ll keep on increasing on mly basis from the parked surplus & of course the liquidity of those 2L Rs. is there.

How can I calculate my saving in Max Gain?

To know your actual saving, first of all please demand a loan amortization schedule from your loan serving branch & now for each month compare the scheduled interest outgo as per your loan amort. schedule & the actual interest outgo.

What should I do to maximize the savings in Max Gain?

If you are paying your EMIs from SBI’s SB account, you can maximize your benefits. How? here it goes. Say 15th is the EMi date on which EMi amount is debited from your SB acct. Now in a normal home loan, people ‘ll keep at least 2-3 months’ EMI amount as buffer in SB account. but in case of Max Gain, you do not need to keep buffer in SB account. Keep this buffer amount also in your MG account along with your routine surplus amount. now use the power of netbanking of SBI for your own good & create a schedule transaction of your EMI amount 28951 Rs. (in the above example) to be transferred on 13th of every month from MG account to SB account. At a time you can schedule for next 12 months by using standard instruction. So it’s technology that’s helping you.

I can transfer money to MG account from my existing netbanking enabled SB account but reverse is not happening. why?

The answer lies in the fact that Netbanking transaction rights on your MG account is not enabled yet by your loan serving branch. if final disbursal is done, you can apply for transaction rights. if only partial disbursement has been done, sorry, you can’t apply for transaction rights till final disbursal.

Is it mandatory to purchase property insurance & life insurance along with Max Gain?

Having property insurance as well as sufficient life insurance is compulsory but purchasing the same from SBI’s sister cos. like SBI General ins. & SBI Life ins. is not at all mandatory. If you feel that policies are being cross sold to you to exploit your position (home loan seeker), please contact the AGM of your local RACPC where your loan application is under processing.

Is SBI charging higher processing fee for Max Gain?

No, as on date there is no differentiation in fee for term loan & Max Gain but SBI reserves the rights to charge different fee.

Can I claim section 80C principal repayment benefit for the surplus amount parked in Max Gain?

The answer is NO. Only the regular principal repaid by you from your EMI as part of your loan amortization schedule is available for tax benefit under section 80C. the parked surplus amount is liquid money & you can withdraw it any time, hence it’s not considered as actual repayment of loan & thus not eligible for tax benefit.

Can I avail cheque book & ATM card for my Max Gain account?

Yes, as & when you‘ll demand these, SBI ‘ll offer you the same. In case you are already holding an SBI SB acct. linked ATM card, you have the option to link your MG acct. also with this existing ATM card.

Can I enroll my MF SIPs in Max Gain?

Yes but do note, there should be a surplus balance i.e. available balance on the date of SIP, else your ECS or SI mandate ‘ll bounce.

Can i pay for my utility bills, credit card payments, online shopping from Max Gain?

Yes, you can do all this & more. In fact it’s in your best interest that you treat your MG account as your primary money parking account & route all your transactions through it so that money is lying there for maximum possible time & thus helping you to bring down your interest outgo.

I used my MG account ATM card to withdraw cash from other bank’s ATM & I was charged the money very first time in the month. Why?

The reason is, as per RBI’s circular 5 transactions on other banks’ ATM are free only for SB account & in this case, you forget the point that your MG account is not SB account. it’s an overdraft account.

For an imaginary situation, my loan amount is 30L Rs. & parked surplus amount is also 30L Rs. Does it mean, my loan is closed & I can claim my property papers from SBI?

No, your loan is not closed. Only interest outgo ‘ll become zero & EMI ‘ll remain continue as it is. Yes the interest part of your EMI ‘ll keep on accumulating in your MG account. If you want to close your loan at this point, you w’d have to inform SBI in written & now SBI ‘ll adjust your parked surplus amount towards the outstanding loan amount. you ‘ll lose the liquidity of your money but loan ‘ll be over & now you can get your property papers back.

How can I transfer my loan from other banks to SBI Max Gain?

For loan transfer, first of all contact your existing lender & ask for following things.

1. Loan Account statement from day one.

2. List of Documents, which were submitted by you at the time of availing original loan. In day to day language of bankers, it’s called LOD.

3. As on date outstanding loan balance with applicable interest, penalty & any other fee to close the loan.

Now contact, the nearest SBI Branch (if you do have an existing SB account with SBI, it’s advisable to contact there for ease of operation). Inform in that branch that you want to transfer your loan from existing bank to SBI Max Gain. fill the application form, submit the necessary papers & SBI’s RACPC ‘ll do the back gorund job.

Once SBI is ready to accept the transfer, it ‘ll issue you a sanction letter of the loan amount & ‘ll ask you to go for loan related agreement documentation work with SBI. If you are not having property insurance, SBI may ask to purchase one. Same ‘ll be the case for your life insurance. Once legal documentation is over, the cheque of the loan balance ‘ll be issued directly into the name of the bank in question. After the amount is credited to your existing bank, within next 20-30 days, you ‘ll get the original documents submitted by you, from the existing bank. Now you w’d have to submit these documents to SBI. In some states like Gujarat, Maharashtra, Karnataka, SBI may ask to go for registration of mortgage deed on your property in the office where your property was originally registered in your name.

Comparison of SBI Max Gain to Normal Home loan

|

SBI Max Gain |

Normal Home Loan |

|

Liquidity of your part prepayments is there |

No Liquidity. Money is gone for ever, once you prepay. |

|

A bit complex to understand |

Easy to understand |

|

For people who can generate regular surplus amounts |

For people who can only manage regular EMIs |

Click here to know the real life example of Mr. Sudhir S for SBI Max Gain

Do you feel, this article was able to answer your all queries related to SBI Max Gain? Was this article helpful for you to understand the overall concept of SBI Max Gain home loan? Please feel free to ask for more help.

Thanks for the wonderful information you have provided in this article. I really helped me to clarify few doubts 🙂

Though i have one below question :

1. In SBI Max gain loan, EMI for a particular month gets credited to the account and at last day of every month, the interest component gets debited. But in this case EMI amount will be constant? And also how the interest which gets debited at the end of the month is calculated?

On the EMI credit date, the Principal part of your EMI is adjusted towards loan and your DP comes down. On the last day of the month, interest is calculated on daily BB and charged to your Max Gain account.

Thanks

Hi Ashal,

Yes I have noticed that my drawing power is not reducing. Should it be actually reducing as the principle gets deducted every month?

The surplus is just equal to my EMI which I remove after the EMI gets deposited to my Max Gain account.

Dear Sushant, your Drawing Power should come down with every passing month. Please contact your loan serving branch to report the matter. Although you are not losing anything in terms of Interest outgo on the loan but yes, the Drawing Power should come down every month.

Thanks

Ashal

Hi Ashal,

Please refer the below details:

Book Balance 28,271.57

Available Balance 24,41,149.57

Limit 24,12,878.00

Uncleared balance 0

Drawing Power 24,12,878.00

Currency INR

Rate of Interest (% p.a.) 8.35%

For the last few months my Available Balance is more than the Drawing power.

However, I have observed that my Drawing power is remaining same and not changing for the last few months. Shouldn’t it be reducing every month as the principle amount gets deducted every month when my EMI gets deposited in the account?

Is this a right understanding or am I missing something here?

Your help is much appreciated.

Dear Sushant, do you mean to say, your Drawing power is not changing from 2412878 for last 4-5 months?

On a different note, positive book balance indicates you have more money than the loan value itself. Please remove that extra money as it’s not earning any interest for you and can be used/deployed elsewhere.

Thanks

Ashal

Hi, If the surplus amount in OD account is deceasing the monthly interest then resulting EMI term should also decrease. Isn’t it ? Because decrease in interest eventually results in increase in per month principal amount payment hence the loan repayment should complete sooner than original decided term.

Dear Sanjeev, Please reread the article. The Max Gain or should I say OVER DRAFT home loan products don’t offer Term reduction. Yes, by parking more and more money into Max Gain, your interest outgo is coming down with every passing day. That’s your benefit.

Thanks

Ashal

Really Good Article.

Rgds

Sachin

Thanks

Hi Ashal,

I have SBI MAXGAIN loan. I want to max out my tax deduction on principal payment and approached the current bank manager to pre-pay the amount and considered it for Principal payment.The new Bank manager says it will be not considered as Principay payment under the system. Earlier managers ( it was SBH then) used to reduce my Drawing balance and available balance and give provisional statement for tax purposes. Please let me know how to explain to the current bank manager.

Please ask your branch manager to adjust a sum from AB towards DP permanently. This way, you’ll lose the liquidity of the money but the amount ‘ll be considered for 80C calculation.

Thanks

Ashal

Hi Ashal, Its a nice article. Can you please help me for my SBI MG Home Loan Account. It says account type as OD account as you explained.It shows below details:

Sanctioned Limit: Rs. 13,95,000

Available Balance: Rs. 39,688

Does it say that My Principal amount = Sanctioned Limit. And I can withdraw available balance?

This Loan account is linked to my SBI Joint Savings account and from this account only, EMI gets debited. I have saved Rs. 14 lakh in my linked savings account.

Should I close my Loan now? How can I get this closed online? Thanks.

Dear Sharad, parking of surplus fund in your joint saving account is not giving you the desired benefit. The said surplus amount should be parked in the OD account. Then only you ‘ll save on interest outgo. For better understanding of Max Gain, you may check my 2 YOUTUBE videos.

Thanks

Ashal

Hi,

Thank you for wonderful information.

I am trying to do backward calculation of principal, interest, interest-saved on my maxgain account (RACPC, Shankar Seth, Pune did not reduce my drawing power from Jul-2014. Being out of India didn’t help either. Story for another day).

It seems likely monthly interest rate calculation is not simply (1/12) of interest rate.

Can you tell me if number of days in month matter? Does year is counted as 360 or 365 days? (In finance terms – is it Act/360 or Act/365 or 30/360 etc. in interest rate calculation).

Thank you for kind attention.

The no. of days in a month matters as the interest is charged on daily reducing balance. The interest is not flat 1/12th but 1/365 for every day.

Thanks

Ashal

Hi Ashal,

From where can I get amortization schedule ? I talked to my loan serving branch and they don’t have any clue about it. Will I get it from RACPC center ?

The loan amortization schedule is to be provided by your branch itself. If the people there don’t have an idea, complain to RACPC.

Hi,

Thanks for nice article. I have taken SBI Max gain loan and I have parked around 3 lakh in my OD account now i need to transfer to my savings account, but when I tried to transfer the amount from OD to savings there is no option available in internet banking.

Here I am confused how exactly I can transfer the amount from OD to savings bank account, is only the cheque is available option, please suggest me.

Regards

Anand

Did you get maxgain transaction rights from your loan serving branch? Once you get the transaction rights, you should see the option in fund transfer as debit account as OD account i.e. loan account. Ideally once all loan amount is disbursed and the property is registered, you should go to RACPC branch and they should give you one form (don’t remember the name), that you need to show in loan serving branch, and write an application to give you transaction rights. With in 1/2 days you should see OD account as debit account in fund transfer page.

Dear sir,

I have saving account in sbi and i am planning for home loan.

I have two questions regarding sbi maxgain home loan, which i am planning for my new home.

1. Is Pradhan mantri aavas yojana subsidy applicable in sbi maxgain home loan for mid income group (6-12lakh income) first time home buyers.

2. In Sbi maxgain how interest will calculate during under construction time.

Suppose during under construction first disbursement 6lakh given by bank and suppose i have 5 lakh already surplus in my OD loan account, in this case sbi maxgain will first interest on 6lakh will take from my side and then from that interest taken by sbi over 6lakh interest of 5lakh will be added in my OD account. Is this assumption is correct. Or sbi will ask for interest only over 6-5=1lakh. Which case is correct.

3. For Sbi maxgain home loan if i have taken pre-emi option, means only intrest will be pay during possession, so in this case can i put surplus money in loan account which i get meantime and get interest saving accordingly. If yes, is there any limit during under construction stage for surplus money to be add or no of time money will be add.

Regards,

Atul Jagtap

Dear Atul, SBI is not offering max gain for loans less than 20L now a days. But Interest subsidy is available.

Interest ll be charged only on 1L for your given example.

As of today, if I have X amount in Closing Balance which will get all paid in about 3 months. I am getting sms from Bank for Available balance of Y amount. Does that mean Y is the surplus amount which can be withdrawn even after loan is closed in 3 months.

If Y is greater than X, you are eligible for X-Y as surplus amount to be available post loan closure.

Thanks

Ashal

Hi,

If we do any transcation,transfer money from my max gain aacount to any other bank(net banking).Will there be any commission on each transcation through net banking?Please let me know.

The usual charges for IMPS/NEFT/RTGS ll be there.

Hello Ashal

This article really seems like great education kit for all SBI Maxgain home loan account holders.

My query here is, how could i know how much i saved/ earned by parking money in maxgain account. is there any way for that.

Dear Rajesh, yes you can do it by checking the Google sheet created and shared here by dear Shrikant Bilurkar in Aug 2013. Please check his comment below.

You can also check my two YouTube videos on SBI Max Gain.

Thanks

Ashsl

Hi, I have taken Max Gain loan from SBI and the first owner is my wife. Currently, she does not hold any SBI account whereas I have an SBI account and EMI gets deducted from the same. My question is,

1. Does my wife need to open an SBI account to avail Max Gain benefits or co-owners accounts also works?

2. Does SBI create an account at the time of loan processing or the customer needs to apply for new OD account in SBI?

Your reply will help me a lot just like your post did.

Thanks

Anand

Dear Anand, as your wife is co-owner as well as co-applicant, she is eligible for tax benefit on loan. To pay her share of EMI, she can transfer money from other bank account to your SBI SB account. No need to open new SB account for her. SBI ‘ll open the OD account automatically.

Thanks

Ashal

Hi Ashal,

Currently I am having a home loan with AXIS bank. After MCLR Axis is charging 8.70% and SBI Max gain charges 8.80%. Still it is beneficial to go with SBI Max Gain???

Dear Sachin, that’s your personal call.

Thanks

Ashal

Hi This one is very nice article about SBI Max Gain…

I have two queries:

1 I took home loan in Aug 2016 and rate was 9.45 which is shown as 9.40 in online banking…Now the rate have been reduced but still there is no change in the rate.What to do.

2 Me n my are joint holders in the property and OD account .We opened a savings account on either or survivor basis.Now my wife has issued a cheque with her signature only from the OD account’s chequebook.Will that require my signature also or anyone can sign on the cheque?We are not sure as OD account was opened by the RACPC.Please guide

Dear Umesh, relax. Your loan is already linked with MCLR and in August 2017, you ‘ll get new Rate automatically. Any one of you can sign cheque and it’s valid.

Thanks

Ashal

Dear Ashal,

If my SBI Max Gain (MG) homeloan is for 30L and i park my sirplus amount of 30L there, what happens when my regular EMI amount of Rs 30,000 goes to SBI maxgain a/c by ECS, will SBI reject this EMI by ECS ? or will SBI pay me interest on this sirplus Rs30,000

Thanks

Dear Tapan, SBI ‘ll not reject EMI. You ‘ll not earn any interest on extra amount. It’s in your own interest to remove the surplus amount immediately through netbanking.

Thanks

Ashal

Hi Ashal,

With the change in interest rare through MCLR , is this worth to switch over ? for my loan ROI is 9.40%. If I change over it will become 8.80% considering I am opting for 1 year review period. Not sure bank charges any amount o switch over. Though I see the difference does it help us on long term basis ?

Please wait for Feb MCLR and switch after that. Yes, you w’d have to pay a switch over fee.

Thanks

Ashal

Is it right to wait for Feb MCLR?

To my understanding, once we switch to MCLR by paying a switch-over fee, your spread gets locked. – Please correct me if I am wrong!

SBI lowered MCLR but increased the spread on Jan 1st.

Eg.,

MCLR and spread before 1st Jan – 9, 0.25

MCLR and spread after 1st Jan – 8, 0.65

Hypothetical MCLR next year = 7.5

if I had switched to MCLR before Jan 1st my interest rate would be 9.25 but would reduce to 7.75

If I switch to MCLR now, my interest rate for one year would be 8.65 but change to 8.15

If we wait till february we may benefit for this year if interest rate reduces, but what is the guarantee that spread is not increased further?

Dear Srikar, if you feel, waiting may prove costly to you, please feel free to switch now.

Thanks

Ashal

Hi Ashal,

I am holding a SBI Max gain home loan account and i see that the interest is not decreasing every month. Below is the snippet:

Value Date Description Ref No./Cheque No. Debit Credit Balance

5-Jan-16 BULK POSTING-BY SALARY– 31,094.00 -29,68,669.00

31-Jan-16 DEBIT INTEREST— 23,732.00 -29,92,401.00

5-Feb-16 BULK POSTING-BY SALARY– 31,094.00 -29,61,307.00

29-Feb-16 DEBIT INTEREST— 22,149.00 -29,83,456.00

5-Mar-16 BULK POSTING-BY SALARY– 31,094.00 -29,52,362.00

31-Mar-16 DEBIT INTEREST— 23,602.00 -29,75,964.00

5-Apr-16 BULK POSTING-BY SALARY– 31,094.00 -29,44,870.00

30-Apr-16 DEBIT INTEREST— 22,784.00 -29,67,654.00

5-May-16 BULK POSTING-BY SALARY– 31,094.00 -29,36,560.00

31-May-16 DEBIT INTEREST— 23,476.00 -29,60,036.00

6-Jun-16 BULK POSTING-BY SALARY– 31,094.00 -29,28,942.00

30-Jun-16 DEBIT INTEREST— 22,669.00 -29,51,611.00

5-Jul-16 BULK POSTING-BY SALARY– 31,094.00 -29,20,517.00

31-Jul-16 DEBIT INTEREST— 23,348.00 -29,43,865.00

5-Aug-16 BULK POSTING-BY SALARY– 31,094.00 -29,12,771.00

31-Aug-16 DEBIT INTEREST— 23,286.00 -29,36,057.00

6-Sep-16 BULK POSTING-BY SALARY– 31,094.00 -29,04,963.00

30-Sep-16 DEBIT INTEREST— 22,484.00 -29,27,447.00

I do not understand why interest repayment is varying every month from and 23K to 22K and back to 23K.

In above period I have not parked /withdrawn any amount.

Can you help please? If this is normal in sbi max gain accounts?

31094 is my EMI on 5th of every month.

Dear Ankit, look closely, your interest is actually coming down. In jan 16, it was 23732 and in Aug 16, it’s 23286. Please look into the interest debit months and the no. of days in that month. Jan, Mar, May, Jul and Aug are having 23K+ interest on 31 days in these months. Other months are having just 30 days, hence lesser interest.

Thanks

Ashal

Hi Ashal,

I have one more questions related to amortization principal calculation with MG. I know they are calculating interest on daily basis. But are they using same method during their amortization schedule as well ? or they will go with monthly basis.

say for 30L with interest a rate of 10%, when calculating for month of Jan (consider previous closing amount as 30L)

which method are they using to calculating principal part in amortization schedule

method 1 : EMI – 30L *10/12/100

method 2 : EMI – 30L*10*31/100/365

(subtracting interest part from EMI. Method 1 use monthly and method 2 use daily interest calculation )

Appreciate your help here.

Dear Anoop, it’s daily reducing interest calculation in SBI.

Thanks

Ashal

Dear Ashal,

So the principal will calculate using method 2 above, correct ?

Yes.

Thanks Ashal

Hi Ashal,

will you able to provide me a sample amortization schedule if you have, I will drop an email to you .

thanks

Anoop

Dear Anoop, the loan amortization schedule – a google sheet is shared by one reader in below comments – named as Srikant Bilurkar.

Thanks

Ashal

Hi Ashal,

Thanks for the spreadsheet details. I found that the interest calculation on that sheet very interesting. take imaginary values as

Loan amount :30L

ROI :10

EMI : 40000

EMI date :5th

The sheet calculating interest like below for month of Jan

(3000000 × 10× 31)/36500 – (40000 × 10 × 27)/36500

From this what I understood is calculate daily interest on opening balance, then calculate interest on EMI amount starting from EMI date to end date and reduce this value from first.

Am I correct here ?

Dear Anoop, the interest is calculated on daily book balance. Once EMI is credited, the interest part of EMI becomes available balance and thus book balance is reduced and hence less interest till last day of month.

Thanks

Ashal

Hi Ashal,

Yes, that I totally understood and that is why I asked the question. If you check amortisation calculation on the excel you have mentioned, it is reducing total EMI interest from previous BB interest. But we have to deduct principal part from emi and then calculate interest.

So do you think that excel calculation is correct. Can you please verify the same with an official amortisation sheet from SBI ? If you have any please send it to me so that I can verify

Hi Ashal,

Thanks for you reply to my previous post. I am trying to do some math here and can you tell me if my below understanding is correct.

Suppose, my loan amount is 30,00,000 and EMI is 30,000 out of which interest is 25,000 and principal is 5000. EMI date is 5th.

Now, consider month of Jan. On Jan first my DP is 30,00,000. Jan 5th, my EMI will credit to the OD. So upon EMI credit my AB will be 30,000. principal part will be deduct on same day from AB.

At end of Jan 5th,

DP = 30,00,000 – 5000 = 29,95,000

AB = 25000

BB = 29,95,000 – 25000 = 2970000.

Will interest calculate on this BB 2970000 for next 26 days or will it calculate on 29,95,000 ? (After deducting principal )

Can you tell me what will be my DP, BB,AB on Jan 6th (Consider I am not depositing any amount as surplus) if above calculation is not correct ?

Once again thank you for all your help here

Regards,

Anoop

Dear Anoop, yes from 5th to 31st Jan, interest is calculated on 2995000 – AB = 2970000.

Thanks

Ashal

Thanks Ashal

Dear Ashal,

So in MG choosing an early EMI date will help us save more interest . Because the interest part of EMI will available in AB for days. Selecting EMI date as 5th will helps to save more interest than selecting EMI date as 10th. Am I correct ?

Dear Anoop, yes, having an early EMI credit date ‘ll result in more saving.

Thanks

Ashal

CAN EMI IN MAXGAIN LOAN ACCOUNT BE CHANGED, IN ORDER TO TAKE THE MAXIMUM BENEFIT OF PRINCIPAL AMOUNT EXEMPTION UNDER 80 C . AS SURPLUS PARKED IN MAX GAIN ACCOUNT DOES NOT PROVIDE ANY BENEFIT OF PRINCIPAL PAYMENT

Dear Tanuj, Yes, you can change your EMI. Please contact your loan serving branch to increase your EMI.

Thanks

Ashal

Hello Ashal, I learnt that for Maxgain changing emi do not affect principal as it is fixed based on loan term and goes per amortization unless we totally modify tenure on paper.

also any inputs on having excess surplus how to adjust drawing power in small chunks permanently. any minimum rules or limits for the same on max gain?

Dear Sandeep, to get the effect of Higher EMI, you need to contact your loan serving branch for change in loan amortization schedule.

Once your AB = DP, just start transferring your EMI from maxgain on credit date itself, to keep book balance zero.

Thanks

Ashal

Hi Ashal .

My Maxgain account is taken based on base Rate . Now I read that interest rate calculation is based on MLCR . I see that the interest rate in my account is not changed for past one year (still at 9.4) .

Will the old home loans get the benefit of the rate cuts ?

Thanks

Ajay

Dear Ajay, to get the benefit of MCLR, you need to apply for linking to MCLR instead of base rate.

Thanks

Ashal

Hi Ashal ,

I have a max Gain Loan taken 3 years back . After the interest rate regime has moved to MCLR calculation , I see that interest rate has not changed for my account . (at 9.4 % now)

Could you guide on what needs to be done to get the interest rate reduced ? For the pre MCLR home loans , how is the interest rate reduction transferred to the customers?

Thanks in advance for your reply .

Dear Ajay, please contact your loan serving branch to get the conversion from base rate to MCLR.

Thanks

Ashal

Hi,

Last month i transfer 100000 rs from my saving account to my home loan account. But only 89420 rs credited in my home loan account and other amount credited in maxgain suraksha account.

I checked today my maxgain account. Here 10781 rs debited and it’s transfer to cash management product.

What is this cash management product and why they are debited.

Please help me.

Suraksha account meant for home loan linked term plan, whose prem. is paid as part of your home loan. To keep the matter simple, pay off the Suraksha amount in full to save on interest outgo towards prem.payment under loan.

Thanks

Ashal

Hi Ashal,

I parked 2.1L.

31-Aug-2016 DEBIT INTEREST 45,466.00

29-Aug-2016 BY TRANSFER 2,00,000.00

25-Aug-2016 BY TRANSFER 1,000.00

11-Aug-2016 BULK POSTING BY SALARY 67,546.00

Available Balance is 1,63,496.00.

Why is my AB less than 2,00,000? It was approx 28,000 before I transferred the 2,10,000.

Thanks,

ST.

The AB is less on account of Interest payment (debit).

Thanks

Ashal

I have a question, I had maxgain home loan account for which I have prepaid the money. I have taken this home loan in join accout with my wife. While closing the home loan, branch manager told me that we both need to come for termination of the agreement. As we are not in the same city, it would be difficult for both of us to in home branch. Is there a way that we can close our loan from other branch or my wife can give me a power of attorney.

Dear Sandeep, loan closure does require signature of both applicants, hence presence of both is required. For Power of Attorney thing, please cross check with your loan serving branch.

Thanks

Ashal

Hi Ashal,

Thanks for the wonderful article which provides great insights and helps us all out with our SBI max gain accounts.

I have been having loan thru the SBI MaxGain since June 2015, and all my EMI’s were deducted from my SB account with SBI on 09th of each month, however, EMI deduction did not happen today for some reason.

My savings acount has enough balance for deduction of the EMI though.

Can you please suggest further course of action that i adopt now ??

Thanks in advance.

Regards

Dear Anuj, Please contact your loan serving branch.

Thanks

Ashal

Hi Ashal, Very good article. Below is the status of my SBI MG HL account. (My Actual Loan amount was 17L, I prepayed some and below is the present status).Now I am paying 21K as EMI every month. If my AB = DP, I have to continue my EMIs ryt ? So everymonth emi 21K i will pay and the same 21k will come to AB ? so that i can take that 21 k?

Account Number 000000XXXX

Description SBI H L MAXGAIN OD (APR15)

Name XXXX

Book Balance -8,15,169.00

Available Balance 2,70,620.00

Limit 10,85,789.00

Uncleared balance 0.00

Drawing Power 10,85,789.00

Currency INR

Rate of Interest (% p.a.) 9.35%

Lien Amount 0.00

As per your account data above, you need to park 8.15169 Rs. more as on date to keep that EMI withdrawal thing going.

Thanks

Ashal

Dear Sundar, yes, once your book balance is zero which is DP = AB, you can do that EMI removal thing.

Thanks

Ashal

Hi,

A very helpful article with perfect illustrations.

Previously I had taken “Smart Home Loan” from HSBC and “Home Saver Loan” from Standard Chartered Bank.

Both of them worked exactly in the way you have explained here.

Recently I had to take a loan from Canara Bank and later got it transferred to Citibank.

The name of the loan I have taken in Citibank is “Citibank Home Credit Fast Track”.

I am feeling that, this is working in slightly different way.

They have given me a Current Account and the EMI gets deducted from the amount parked in this account. They told that, the threshold is Rs.1 Lakh and the extra amount is transferred to OD account – the outstanding will come down by that much.

So, I transferred Rs.3 Lakh to this account. In my transactions, I see that, Rs. 2 Lakh got debited and transferred to OD account on the same day.

But, in my account login, I don’t see the OD account at all!!

So, I am confused.

Do you have any info on this? It will be great if you can write similar article for Citibank account also.

Also, they have one more loan called “Citibank Home Credit Vanilla”, which also has OD facility and interest saver.

You can include this also in your article and compare all this with SBI Max Gain.

Thanks,

Narendra

Please contact Citibank to get access to OD account under same login id.

Thanks

Ashal

Dear Ashal,

From the SBI Maxgain Acct statement from the bank website, debit of monthly interest is visible as a monthly entry on the last day of the month. Overall reduction in Principal (till today) can be calculated from the current Drawing Power. How can we calculate / know the amounts of monthly principal paid back (for every previous month) from the account statement?

Thanks in advance.

-Navneet

Dear Navneet, you need to download mly statement or keep track of your drawing power before and after emi credit.

Thanks

Ashal

Ashal, does drawing power (principal) change is updated on emi date or end of month ?

Dear Sandeep, the DP is changed on EMI date.

Thanks

Ashal

Dear,

I have a max gain account since 2013. Now I have parked sufficient funds in it so that the book balance is now positive. Do I still have to maintain amount for EMI in other account from where it gets debit. I plan to keep the amount parked permanently and don’t intend to withdraw.

Dear Babar, Yes. You need to keep the balance in EMI debit account. Once EMI is credited to your Max Gain account, you can immediately transfer it back to any other account of your choice.

Thanks

Ashal

Hi Ashal,

Nice to read this blog and seeing your sound advices. I took a SBI Max gain account in 2014 with 50L loan approval for an under construction flat. I am yet to get the possession which is due this dec, 2016. Till now around 35L amount has been disbursed to the builder and the pending 15L will be enough to make 100% payment for the flat. Now i am in need of another 12L for interior work, for which I need your advice to see which option is feasible –

Want to apply an advance loan from my Provident Fund account to partly repay the home loan ( have sufficient fund for 12L ) and i already completed 10 years of service contributing to PF.

Option 1 : Can I withdraw this money post 100% loan disbursal to builder and possession since it is an OD (Maxgain account ) ?

If yes Post 100% loan amount disbursal how much more days will it take for me to be able to withdraw any surplus parked money from my max gain account ?

Option 2: If withdrawal doesn’t work post possession as well for the PF transferred money. Then should i go for a Top Up loan from SBI again for 12L. How much long process will it take and will the interest rates be higher than my home loan interest rate ?

Assumption taken PF advance will be paid directly to SBI loan account only ( and not to my personal account ) since home loan account is active. If there any other options as well please let me know.

Dear Sarath, Contact SBI for top up loan.

Thanks

Ashal

Hi Ashal,

I have sent you an email for some confusion on my Maxgain loan with attachments. Please advice me on the same.

Thanks,

Peeyush

Dear Peeyush, Replied your mail.

Thanks

Ashal

Hi Ashal,

Can you clarify the following

1) can I withdraw the total amount from available balance(which includes interest accrued on surplus amount deposited) at any point Or am I

entitled to withdraw only the surplus amount I deposit ?

2) Assume my total tenure is 10yrs and i have added some surplus amount to my OD account which made my book balance zero at the end of 5th year.

If the book balance is zero, ideally the EMI will not have any interest component. In that case, what happens to the EMIs that I pay from 6th year

to 10th year (till account closure time)? what will be my available balance at the end of 10th year and can I withdraw

total available balance on liquidation date and collect my registration papers?

3) Am I still allowed to add surplus amount to the OD account though my book balance is zero? In this case, what happens to the interest acrued on

surplus amount?

4) I will ensure that I always maintain surplus amount in my OD account. So can I opt for EMI deductions from my maxgain OD account iself ?

Dear Ashok, the answers for your queries.

1. You can withdraw, full Available balance.

2. EMI ‘ll run as it is, the interest part of EMI ‘ll be added over and above in existing AB and thus you need to withdraw immediately, to keep your BB zero. Else your BB ‘ll also become positive.

3. Once your BB is zero, you should not add more money as positive BB ‘ll not earn any interest for you unlike a SB account.

4. NO. EMI deduction can happen from SB account only.

Thanks

Ashal

Dear Sir, I have missed my this month(May) EMI – occuring on every month 5th – since my saving account did not had sufficient balance. I have noticed this today only.

1. Please let me know how to repay this EMI.

2. Today, I have transferred EMI amount from SB account to Maxgain account. Is it take care of this missed EMI or I have to visit branch for the same. (Pl. note that I am staying in Mumbai and Maxgain account branch is in Pune).

Kindly advise.

Dear Rajendra, relax. Please contact Pune Branch over phone to get the adjustment of principal amount from the amount parked by you late.

Thanks

Ashal

Hello Ashal,

SBI issues final interest certificate at the end of FY. When I checked the total of principal payments made till date (from the starting of EMI), it doesn’t matches with present Drawing power.

Could you please guide on this issue.

Thanks in advance.

Ajit

Dear Ajit, please contact your loan serving branch.

Thanks

Ashal

Hi,

I have taken a maxgain loan and have got some amount already disbursed. (20L out of 50L loan amount).

I am already paying EMI on it.

My question is –

Q1 – I am from Karnataka. During the property registration, If I want to add my wife as co-owner, do I necessarily need to add her name in the loan co-borrower as well?

Q2 – If yes, then what all are the documents needed to get my wife added as a co-borrower the SBI max-gain loan. As I am recently married, I don’t have my marriage certificate ready yet. Wedding card and photos are there.

Q3 – If I add her as co-borrower and in registration if add keep her as primary co-owner, will I get inetrest rate relaxation now?

Thanks in advance.

Dear Manish, here are the answers.

1.Yes

2. Her KYC docs.

3. There are only co-owners in property unlike bank accounts or demat accounts, where the concept is of primary and secondary owner.

Thanks

Ashal

Hi Ashal.

Since SBI does not issue a debit card for max gain can I link my savings account debit card with the OD account?

If yes what is the procedure for the same and what option should I use while withdrawing money or for merchant payments.

Dear Sushant, please contact your loan serving branch for the same.

Thanks

Hi Ashal,

Bank associates said that this cannot be done since Maxgain does not have ATM facility.

Is this information true? If not how do I escalate this issue and get my debit card linked to my Maxgain account?

Thanking you in advance.

Sushant

Dear Sushant, earlier ATM was offered but now, SBI has withdrawn it. It seems, as many other people are complaining the same issue.

Thanks

Ashal

Hello Ashal,

Is there any limit on amount we can withdraw from OD account? How frequent we can transact from OD account?

Thanks.

Dear Mahesh, your available balance is your limit to withdraw. You can do any no. of transaction in a day or week or month, just like you do in your SB account.

Thanks

Ashal

Hi Ashal !

Thanks for Informative articles due to which finally i shifted my Loan from HDFC to SBI .. few Questions :

1. How long does it take for OD A/C to be reflected @ SBI online

2. Will I Get ATM card / cheque Book for OD A/C ; if yes from whom should i take it —– My SB branch & RACPC branch are different !

3. My EMI will be debited from my ICICI A/C — as told by loan office — then where does SBI SB A/C comes in picture

Dear MMsingh, here are answers.

1. If your OD account has been created, it’ll be reflected immediately in your existing netbanking.

2. You can link existing SB account’s ATM card. Yews, you ‘ll get separate cheque book for OD account.

3. You need to ask to SBI to get the EMI debited from your SBI SB account. If EMI is not happening from there, your SBI SB is not in picture.

Thanks

Ashal

Hi,

If I take loan of 10L and at any given point of time park 11L in the account. Will I get any interest in 1L surplus fund?

-Regards

atul

Dear Atul, no, you ‘ll not earn any interest on this extra 1L amount.

Thanks

Ashal

Question: If the savings account from which EMI is automatically taken has less balance on an EMI date, do they take the EMI from overdraft balance automatically? If not, can that be set up? That can be a good insurance for not missing EMIs. Thanks.

Dear Sanjay, this ‘ll be counted as EMI bounced. To avoid this, you need to set up EMI amount 2-3 days before, getting credited from OD account to SB itself, through SBI netbanking.

Thanks

Ashal

Hi Ashal,

Thanks for this article. I have a doubt, recently I transferred my homeloan from a private bank to SBI and today I visited the branch to get transaction rights and to apply for cheque book and debit card. The staff in the branch said that now SBI is not issuing debit card for maxgain loans, is it true? Also as a trial I moved some fund to OD account, though the amount got credited in the account, the balance is showing as zero. Any clue why it so..?

Dear George, yes, new accounts are not offered debit cards. Please send me your account statement in exl. sheet.

Thanks

Ashal

Hi Ashal

I have some queries regarding full disbursed MG account:

(1) I have applied jointly for loan with first applicant my wife; a housewife, but only wife name is displaying in the OD account. Can I get the benefit of tax rebate on home loan?

(2) We have applied for 20 lakhs but final disbursement was only 189228, but still in OD showing available balance 107712. In which amount EMI payment will be done?

(3) How to get online access to transfer of money from OD to other saving account?

(4) One more account listed in my wife’s online saving account Max gain suraksha, where Limit-48780, Drawing power-9756, rate of interest -10.3% and outstanding amount -9756 is displaying. Is it insurance premium account?

Please clarify the above details.

Thanks & regards

hemant

Dear Hemant, here are the answers to your queries.

1. Yes, you can, if you are also the co-owner of the property in question.

2. EMI ‘ll be same like 20L loan amount but you ‘ll be paying less interest as disbursed amount is less than 20L.

3. Please contact the loan serving branch.

4. Yes, it’s insurance prem. account.

Thanks

Ashal

Thank u very much for your clarifications.

Can you help me to guide for the following issues:

(1) Bank issued Home loan Suraksha insurance in the name of my wife in place of my name. Bank told, we will cancelled it after one month and you can take term insurance which is linked with home loan. How it will affect me in term of benefits? It is a fault of bank, can I reclaim the deducted premium amount?

(2) EMI deduction to be done from SB account or OD account? How can link the OD with SB so it get sufficient balance from OD just before the date of EMI deduction?

(3) In the OD account, only first applicant name can be display? How can I add my name into the OD account so it can display?

Thanks & Regards

Hemant

Dear Hemant,

1. Cancel now. Don’t wait for 1 month.

2. EMI ‘ll be debited from SB account. Through netbanking. The SB account and OD account under a common login ID should be there.

3. Joint applicant’s name remains there in records, no reason to worry.

Thanks

Ashal

Dear Shri Ashalanshu

I have requested in written to cancel my insurance on 6th Feb at RACPC but still it is active. When I complained then bank official replied that we can not do anything till sbi life returned back the cheque.

In between time there is deduction of interest on paid premium showing in the account. When I contacted with SBI life they confirm me that he sent the cheque.

My question are

(1) How can get the extra debited amount of interest?

(2) Can I linked ICICI term insurance with this home loan?

(3) I got one letter from SBI to take properties insurance which having about 16500 one time premium. Is it mandatory to buy the properties insurance ?

Thanks & Regards

H V Sharan

Dear Hemant, where is the cheque amount? As the prem. has been paid by SBI as part of loan and still the money is not repaid, interest is due validly.

Thanks

Ashal

Hi Ashal, I want to know how to reach out to you via email. Have a basic query on life insurance as well as SBI max gain account.

Thanks Karthik

Dear Karthik, please check your inbox.

Thanks

Ashal

Hi Ashal,

Thanks for the detailed information.

I would like to clarify two points here.

1. Does the interest calculated on monthly basis or daily basis ?

consider the case 2 you have mentioned above.In that case after parking 2L, the EMI reduced to 23334 (considering 28L as outstanding). But does the date which I deposit 2L matter here ? Suppose If I park this amount on 21st of a month, how the interest will be calculated ? is it like for 30L for 20 days (1 to 20) and 28L for 10 days ?(21 to 31) ?. If I park another 1 L on 25th of same amount the calculation change like below ?

1 to 20th – 30L

21st to 24th – 28L

25th to 31st – 27L ?

2. When OD=AB, how the calculation changes ? As per the explanation, there is no change in tenure of EMI amount. Take a scenario , we have an amount 2L and now OD=AB and remaining months in tenure is 10 months.

In this case does EMI will be same as earlier ? In that case for all the remaining 10 months, interest deducting from me will be available in AB. does this correct ? that means bank is actually taking interest through my EMI and deposing it to AB?

Appreciate your help here. I am planning to move my home loan to SBI and I am trying to understand it ?

Dear Anoop, here are the answers.

1. Interest is calculated on daily basis.

2. Once your AB=DP, BB is zero, your loan is running now on zero interest rate. On the date of EMI credit, yu can immediately remove the excess money from account to make BB zero.

Thanks

Ashal

I and my wife had taken a joint SBI Max Gain Home Loan. This was about 1.5 years back and then suddenly yesterday I can see the following against my OD account

– a transaction of 40K against for premium against SBI General

I don’t understand what this is about. Could somebody help?

Dear Sriram, this is the property insurance prem. bundled with your home loan.

Thanks

Ashal

I have missed my EMI – occuring on 10 Dec 2015 – since my saving account did not had sufficient balance.

What do i need to do now ?

Dear Anand, don’t worry, please pay the EMI now along with the extra amount for the interest on interest to be charged from you for 2 months.

Thanks

Ashal

Hi Ashal,

I have missed my EMI of my Maxgain Home Loan to be paid on 10th April, as I didn’t have enough funds. After calling SBI customer care they told me that I will have to go to branch to do the missed EMI

I wanted to know

1. Some banks initiate the EMI transfer next day if EMI date is missed, does SBI do it as well?

2. if I transfer it today, 11th April manually through netbanking, will it be considered as payment towards EMI, or it would be considered as surplus amount parked?

3. Also, are you aware of the charges need to be paid for missed EMIs?

Thanks in advance,

Dear Charudatta, relax. Please use NEFT and transfer your EMI today from SB account to Max Gain account. In case, you are still short of money, please transfer as and when you are ready with the money.

Thanks

Ashal

Hi Ashal,

I think there is an issue with how my MaxGain has been setup. Can you please check?

Book Balance -62,18,463.50

Available Balance 1,81,536.50

Limit 64,00,000.00

Uncleared balance 0.00

Drawing Power 64,00,000.00

Lien Amount 0.00

Loan Sanctioned – Aug 2015 (fully disbursed for loan amount of 64 Lakhs in Aug 2015)

The apartment is a secondary sale – so there was no part payment / disbursement involved. I have been paying full EMI payments from Sep 2015 (Rs. 61,005.00).

Every month, there are two transactions that I see – EMI amount is credited to the OD account on the 5th of every month. On the last day of the amount, there is a debit for the outstanding interest amount.

I see no debits towards principal. I think it is also reflected in the Drawing Power. Is there an issue in the way my account is setup?

Dear sriram, please contact loan serving branch and ask there for any Moratorium if any. it seems you have availed loan under Yuva category or SBI staff has put it that way and that’s how a moratorium is there. Due to this Moratorium, your principal is not getting adjusted.

Thanks

Ashal

Thanks Ashal – will do. Happy New Year!

Hi Ashal,

My SBI HL Maxgain account EMI is going on for last 8 months, EMI date is 5th. I wanted to know whether I can pay the same EMI amount by online transfer to OD account before 5th, say 1st? in that case, will SBI stop ECS on 5th automatically and not deduct EMI amount from SB account? Will I be able to save some small amount of money due to advance payment before 4/5 days?

Thanks & Regards,

Rabin Prusty

Dear Rabin, NO. Such direct transfers ‘ll not be considered for EMI. It’ll be treated as regular surplus fund parking by you.

Thanks

Ashal

Thanks Ashal…

Hello Ashal, thank you very much for this nice info.

i already have my MAXGAIN account, now i am struggling to get my TAX certificate to get tax exception from office.

SBI and branch says they don’t give any tax certificate for MAXGAIN and i cant see it in my online account too.

my OD is active too, any details on how to get the certificate will be helpful

Dear Subbu, I assume by tax certificate, you are referring to Provisional interest certificate. Please download the same from your netbanking. Although your branch should provide you. If the branch staff is not co-operating with you, please complain the same to SBI customer care.

Thanks

Ashal

Hi Ashal,

I am also looking for Prov. Home loan certificate for my MG loan account. However after login to my SBI account, i am getting message “Housing Loan Interest Certificate for Maxgain is not available online”.

Thanks,

Rajat

Dear Rajat, SBI has allowed Interest certificate download to few accounts, and not to few others. Sorry to say, you are not allowed. 🙂

On what basis, this feature if given or not given, i don’t know.

Please contact branch, to get it.

Thanks

Ashal

Thanks Ashal for info 🙂

Hi Ashal,

Many thanks for a stupendously useful article. I have a couple of questions that i hope you can answer (my MG loan is already operational).

1.Can i transfer my MG loan- it is presently with PBB Jaynagar and the RACPC branch was at Basavangudi. I would like to transfer it to a branch adjacent to me within Bangalore itself (Health city, Bommasandra) as the present location is not accessible. I have emailed the manager and he never replied but on calling he says that the brach cannot be changed as it is of a different region. Is this correct or am i being fed lies?

2. I always have a surplus amount in my MG account- enough to pay off the EMI for the month. Can i set it up so that the EMI gets paid automatically without having to route it through an SB account- t would be simpler and potentially also save a small amount.

3.Is it essential to have a SB account linked to the MG account?

4. Is it possible for both joint account holders to get independent banking access to the account?

Presently I can access the account through my wife’s internet banking (she is shown as the primary applicant).

Once again many thanks for your extremely helpful post and looking forward to your reply.

regards

Dear Robbie, here are the answers for your queries.

1. Yes change in branch as well as RACPC is possible.

2. No. EMI ‘ll be deducted from SB account itself and thus you need to route it that way.

3. A SB account in SBI ‘ll help easy movement of money for EMI ECS. Although it’s not essential.

4. No.

Thanks

Ashal

Hi,

I also have joint MG account. Me & my wife can access through individual SB account login.

You have to link both saving bank account to MG account in branch.

Hope this will help.

Thanks

Rajat

Hello Ashal,

Thanks for a very comprehensive blog on MG.

I have few queries regarding Maxgain Loan. I have transferred my existing home loan to SBI Maxgain 2 months back and 2 EMI’s are already gone.

1) I am really confused on BB, DP and AB. In last 2 months I have deposited 1 Lakh Rs. in this OD account but that amount is not displayed in OD account detailed view. It shows like below –

Book Balance – -3948023

Available Balance – 68582

Limit – 4016605

Drawing Power – 4016605

ROI – 9.35%

No where it is showing the amount I deposited, where can I get that cumulative amount ?

2) When my loan was sanctioned the ROI was 9.75% and from 5th Oct. 2015 it is 9.35%. Which is displayed when I login. Query was will this new ROI will be applicable to my loan automatically from 5th of Oct ? Or I need to go the branch and get it done ?. Will they charge for the same and how much ?

If they dont reduce this ROI on their own what is the reason behind this ?

3) Will the above change of ROI will change my monthly EMI ?

4) My EMI date is 15th of every month. My query was if I change it to 5th of every month will it be more beneficial for me ? Again is this change requires any chagres ?

5) If I plan to deposit surplus amount every month, eventually my BB will be reduced to zero after 5-6 years but DP will remain to say 15-20 lakhs. In that case if I approach to bank to close my loan will they charge me this remaining DP or how ?

6) In case I approach bank to close the loan after 5-6 years when my BB is zero, if my Surplus is more than remaining DP, can I withdraw it at that time ?

Dear prasad, please do check my two youtube videos on SBI max Gain. if you do have doubts, even after videos, I’ll answer.

Thanks

Ashal

Hi Ashal,

Can you please help me with the above queries ? I am waiting for the same eagerly.

Few more updates are –

My initial Loan Amount Sanctioned was – 4061000 on 30th of August 2015 and EMI till now is – 39558 PM. Not sure if it will change after ROI is down to 9.35 % from 5th of Oct.

Do let me know if you want any additional information from my side ? Also it would be good if you can share your email ID.

Thanks and Regards,

Prasad

Dear Prasad, the EMI’ll remain same. There ‘ll be a reduction in loan term against the ROI reduction.

1. Out of 1L Rs. parked by you, a bit has been adjusted towards interest due in August 2015. Remaining amount is part of AB.

2. Your new ROI is applied automatically. Relax.

3. EMI’ll remain same.

4. You may change your EMI date. The difference of 10 days ‘ll result in a small profit to you.

5. No extra charge. You ‘ll lose your liquidity of the amount and same ‘ll be adjusted towards DP.

6. Yes. Actually you should not leave your BB in positive as you ‘ll not earn a single penny on this.

Thanks

Ashal

Thanks a lot Ashal !!!

Yes I have gone through both the You Tube Videos of yours.

Hello, Nice article. My queries are:

1) In my case, I have SBI Home Loan of 10 lac and Parked cash of 10 Lac. Now, bank wouldnt charge me any EMI right? (i.e. Interest on Parked funds = SBI home loan interest ???)

2) Can I park higher fund than actual loan amount? (means Current Loan is 10 lac and parked funds is 12 lacs). In this case, I get interest calculated at Home loan rate on 12 lac (because normal FD rate is 8%)

Thanks for clarifying.

Dear Chaitu, EMI ‘ll be debited even now but there ‘ll be no interest on you as your BB is zero. So you can remove your EMI amount immediately after credit into Max Gain account.

You ‘ll not earn any interest on your parked money. hence no benefit in parking extra 2L.

Thanks

Ashal

Hi Ashal

great info you have provided.. I wanted to know more about the interest earned on positive book balance.

So my Home Loan is 14 Lakhs and I am thinking of increasing the surplus amount to 15 Lakhs to make the book balance positive. In this case, as my understanding goes, EMI will go towards payment of principal amount and interest part will be nullified. However as the book balance is + 1 lakh, will I earn interest at 9.55% on it?

Can I use this OD account to earn interest of 9.55%?

Thanks in advance

Regards,

Amit

Dear Amit, sorry to say but you have not understood the article. There is no positive interest interest earning in Max Gain. So making your book balance positive’ll not earn that 9.55% interest. To understand this thing, please do check my two youtube videos.

Thanks

Ashal

Hello Ashal,

I have a query regarding the available balance in my max-gain loan related OD account. When I checked the available balance yesterday morning, the available amount was around Rs. 16,85,000/-. Sometime during they day or so, SBI has debited an amount of Rs. 24516/- towards interest from this account. Today, when I checked, the available balance is Rs. 16,32,976/-. I am not able to understand how it is this value.

Is there a way to see available balance on a day wise basis? It is not shown even in the monthly statement sent by SBI.

Thanks,

Amit.

Dear Amit, please send me your account statement in excel format.

Thanks

Ashal

HI Ashal,

I am holding SBI Maxgain loan,planning to close my loan since my payment is very near to DP.

1.What are the next steps to close my account?

2.Now my house paper’s are registered with SBI bank name,do i need to re-register back to my name OR do i need to cancel the SBi registration?

3.Do i need to pay any Extra amount to bank to close my account?

4.Where do i approach for all the next steps? RACPC OMR or Bank branch?

Dear Sivaprakasam, when your home loan is running on zero% interest rate, why do you want to close it?

Thanks

Ashal

I have one query. Apologies if it has been answered before. My case is:

Property type – under construction

Loan with HDfc -52 lac disbursed of 60 lac. Approved

Planning to switch to max gain.

If I tell sbi that I want 52 lac as fully disbursed with them, then

can I withdraw funds in this scenario which I parked as surplus funds?. As in, though property is under construction but loan amount is fully disbursed.

Dear Mohit, once the transaction rights are activated, you can move in and out your money freely.

Thanks

Ashal

Hello Sir,

I am replying to this blog again after a year or so as it’s the best source to understand Max Gain. Here is the situation now:

I do not want to “park” money on the SBI maxgain account because I do not want liquidity of that amount. I just want to bring down the loan principal forever by doing prepayment. This is because parking money will just save some interest for me but prepayment will bring down the principal and will be more beneficial eventually. I hope I am right.

I gave the cheque worth Rs 2 lacs to the bank for prepayment purpose. But when I checked the account, that amount was seen in the “Available Balance”. This means that my loan principal is not reduced forever; the money is just parked there.

The officials in the SBI are now saying that I cannot do prepayment unless I am going to pay more than 20% of the principal amount. And they are saying that prepayment can be done only twice in the entire tenure. Is it correct or SBI is misguiding me?

If this is the case, how come Max Gain is beneficial for those who can prepay the loan once in a year or so? When i transferred my loan from HDFC to SBI, I was told that prepayment is allowed.

Dear Amey, why do you want to prepay? Either you prepay or keep parking money in Max Gain, in both cases, the effect same in the form of less interest outgo. Where is the benefit to you?

Thanks

Ashal

I see.

Extra payment towards principal only (i.e. prepayment) will bring down my “dues” (principal) to the bank. It will bring down tenure as well. And that’s why we are advised to prepay any loan whenever possible and close it asap. Isn’t it? How to get this benefit in Max Gain?

Now since this is not allowed, I am earning interest on my “parked” money at just 9.95%. If prepayment means just parking the money there, then I can invest it in the tool which can earn me more ROI. Is it not the wise option?

Please help me understand it better.

Just for sake of discussion, if you do have book balance zero today, does it make any difference to you that loan is running for next 1Y or 20Y?

Thanks

Ashal

Hi Amey,

Max-gain works very differently from ordinary home-loan.

I would imagine max-gain as something like the following(let us put aside emi’s for a second):

Say I needed money(say 2 lakhs) and I approached a friend, he is willing to lend me money but at some rate of interest.

But he says, he will open an account for me and put that money there and I am free to use the money from that account.

He says he will check the balance every day and charge me interest only on how much money I have used up in this.

Let us say I only wanted 10k for a trip, he will only charge me interest on the 10k and not on 2 lakhs.

After the next salary if I put that money back in the account he will not charge me any interest at all.

Now I still have the option to take upto 2 lakhs from the account whenever I need it.

To understand prepayment in this context, it is like telling my friend “Hey I no longer need a 2 lakhs credit line, you reduce it to say 1 lakh”. This is what pre-payment essentially means w.r.t max gain.

Book balance in this scenario is

1. When loan availed – 0

2. When 10kwithdrawn for trip – 10K

3. When 10k re-deposited – 0

If I am charged interest only on book balance, why should there be a hurry to pre-pay the loan?

Whether you want to use this credit line for your expense or other investment is up to you take a responsible decision. Pre-payment is only reducing your credit line

Now re-read the article to understand how emi’s and schedule work with this picture in mind.

HTH,

Srikar

Thank you very much 🙂

Hi Ashul

I’m having a Maxgain account running from last 2 years i tried to match the available balance by adding all the parked amount till now but there is huge difference . Can you suggest me how i can calculate the available balance .

Loan Amopunt : 39.20 Lacs

Book Balance : 3175255

Available Balance : 573962

Drawing Power : 3749217

Dear Sameer, add the EMIs + any extra amount parked by you, in one column of excel sheet. Add the interest debit and debit done by you (if any) and add the reduction in drawing power in another column.

The figure should match.

Thanks

Ashal

Hi Ashul

Not getting what is reduction in drawing power.

I did like this and it is matching :

EMI + Amount Parked : 2318733

Interest debit + debit self : 1573988

A= Difference of above = 744745

Loan Amount = 3920000

Book Balance = 3175255

B= Difference of above = 744745

So A= B

but i want to know how to see available balance – Pls help ?

Regards

Sameer Saxena

Dear Sameer, what was the original Drawing power and current Drawing power? The difference between the 2 is the reduction in Drawing power. This is actual, loan repaid by you. Add into it the Interest paid by you + bank’s extra debit if any. This is all the debit amount to bank. + Any debit made by you.

On credit side, all the extra amount parked by you + regular EMIs.

The difference between credit and debit amount is your available balance.

Thanks

Ashal

Hi Ashal

Thanks i have applied for loan of 40 Lacs but taken only 39.20 Lacs and paid the balance from my self . Current drawing power is showing as 3749217 so shall i deduct it from 40 Lacs or 39.20 Lacs 😦 … not sure . can u pls share your mail ID with sameersaxen@gmail.com so that i can send you the excel of my account statement to check and advise.

Regards

sameer saxena

Hi Ashal,

I have taken a HL on 29th July, on which the EMI’s have started but full money is not yet disbursed.

Because the loan is only partially disbursed, my interest outgo is lower than in amortization schedule.

However, I was expecting the drawing power to be as follows:

DP=OLD_DP-(Principal repayed as per Amortization schedule)+EMI-(Actual interest deducted). which is same as

DP = OLD_DP+Saved Interest as compared to amortization schedule

While BB is showing as per my expectation, the DP is not following the above? Has there been a change in Maxgain home loan policy in April 2015? If not can you help me understand this.

Thanks in advance,

Srikar

Hi Ashal,

I forgot that I had already asked this question on the 2nd video page and you have answered.

However, I forgot to note down the DP after first EMI, so I am unable to correlate if the second EMI has my drawing power adjusted correctly. Will have to check it after 3rd EMI I guess.

BTW thanks a lot for the all the information and responses, its fabulous.

Regards,

Srikar

Dear Srikar, please keep the track of EMI and update me for any problem.

Thanks

Ashal

Dear Stikar, thanks a lot for the detailed answer.

Thanks

Ashal

Dear Sir,

Thanks for the detailed post on SBI MG OD account, i already have an SBI MG account for Rs. 45,00,000/- and am saving on my monthly interest outgo too. My question is on part pre-payment on the on my SBI MG OD account.

Let us assume that i am saving an amount of Rs. 7,000/- per month in my interest outgo portion, now at the end of a financial year i would have saved appx. Rs. 85,000/-, i wish to transfer this Rs. 85,000/- saved as a part pre-payment for my home loan, how can i do this in the MaxGain OD account.

Thanks in advance.

Regards

Anuj Gandhi

Dear Anuj, to prepay partially from the saved interest amount, you need to contact your bank branch. Personally I w’d not prefer to prepay as it ‘ll bring down my liquidity.

Thanks

Ashal

Hi,

I have a question on the sbi OD account and SBI loan account.

I transferred rupees 20k from my SBI saving account to SBI OD account.

This is what happened

19814 was deposited in my OD account

186 was deposited in my SBI loan account(max gain suraksha account)

why is this?

Is this gone happen ever time you transfer money from your saving account to your OD account??

Thanks,

Archana

Dear Archanar, are you having Rin raksha policy? The suraksha account is meant for this policy’s prem. money. Please pay out the whole prem. from your own pocket and close the suraksha account.

Thanks

Ashal

Hi Ashal,

First of all thanks for explaining about MG and its advantages 🙂

I do hold this type of loan account. I can see the following when i login to MG account:

Account open month: July 2012

Full Disbursed in Jan 2014

Now I can see:

Account Number

Description SBI H L MAXGAIN OD (APR15)

Name Mr. MOHAMMED QASIM PATWEKAR

Book Balance -24,88,213.00

Available Balance 0.00

Limit 24,81,832.00

Uncleared balance 0.00

Drawing Power 24,81,832.00

Currency INR

Rate of Interest (% p.a.) 9.75%

Lien Amount 0.00

(in APR 15 I paid extra money to reduce the ROI)

If DP-AB=BB, then in my case it doesn’t true? what is wrong here? Today I transferred 25000 money into this account. What would the figure next time around (7 Sept, as 5th sep my EMI is debited from my another account).

Can you please reply.

Thanks.

In between, you did not pay some interest and that’s the reason of having higher book balance. Now as you have parked 25000 Rs. extra, your book balance ‘ll return to normal equation.

Thanks

Ashal

Hi Ashal,

Thanks for the reply. As far as I know, and I checked all the previous 4 years sheet, nothing is pending from my end, no dues of any kind. What should I do? Is bank statement is showing wrong entries (not possible)?

Thanks,

Qasim.

Dear Qasim, can you mail me your account statement for all these 4Y?

Thanks

Ashal

Hi Ashal,

I’ve sent you the loan statement (to your gmail account). Can you please advise me further on this issue.

Thanks,

Qasim.

I am confused on the MAX GAIN concept. In the above example, Case – 2 Max Gain home loan, it is mentioned as “Your loan term is still 240 months but the saving of interest ‘ll keep on increasing on mly basis from the parked surplus”. So, there is no change in the loan term (tenure) and the EMI. As a max gain user, what benefit I am getting here? When the interest rate is getting reduced, it should be reflect either in the loan term (tenure) or in EMI. Am I missing anything?

Dear Ramkumar, the saving ‘ll be there in terms of less interest outgo.

Thanks

Ashal

Hi Ashal,

My first EMI was deducted on 10th Aug 15.

My OD account before EMI deduction was:

Book balance: -22,70,136

Available balance: 3,52,858

Drawing power/Limit: 26,23000

After EMI deduction (Rs 28141) it is as follows:

Book balance: -22,42,000

Available balance: 3,80,999

Drawing power/Limit: 26,23000

I couldn’t see reduction in my drawing power. Could you please help me in understanding.

I also have SBI life insurance of 41000. So total loan amount is 26,64,000 & Loan disbursed on 26th July.

Thanks

Dear Rajat, please check your drawing power today 11th August 2015 and confirm the reduction.

Thanks

Ashal

Hi,

Thanks for reply. I checked it now, still the figures are same.

Thanks,

Dear Rajat, in that case, please contact Loan servicing branch to do needful in reduction of drawing power.

Thanks

Ashal

I have max gain account in one branch (say Bhopal) & Saving account branch in other location (Mumbai). When I login through internet banking i can see both of my account listed (OD & Saving).

Last week, I went to my max gain account branch (in bhopal) & applied for transaction rights. As per branch the request is processed & they double check it that I have appropriate right to withdraw money from OD account.

However still I am unable to withdraw money from OD account.

Could you please advice what next step I should take to resolve the issue.

Does visiting the saving account branch will help?

Kindly help.

thanks,